It’s a tricky time for the real estate industry. Prices are up, but they’re not “up up.” Also mortgage applications are down roughly 60 percent from their peak in April, and several heavy financial hitters are getting ready to take the money and run.

Thus the “housing recovery” – such as it was – is drawing to a close.

“Who will be left holding the bag this time?” the website Zero Hedge asks.

Um … taxpayers, naturally. Unless of course you think (gasp) those who made bad loans should be held accountable for their decisions – which is kinda hard to insist upon when the federal government mandates so many of those loans (like it now mandates us to purchase health insurance).

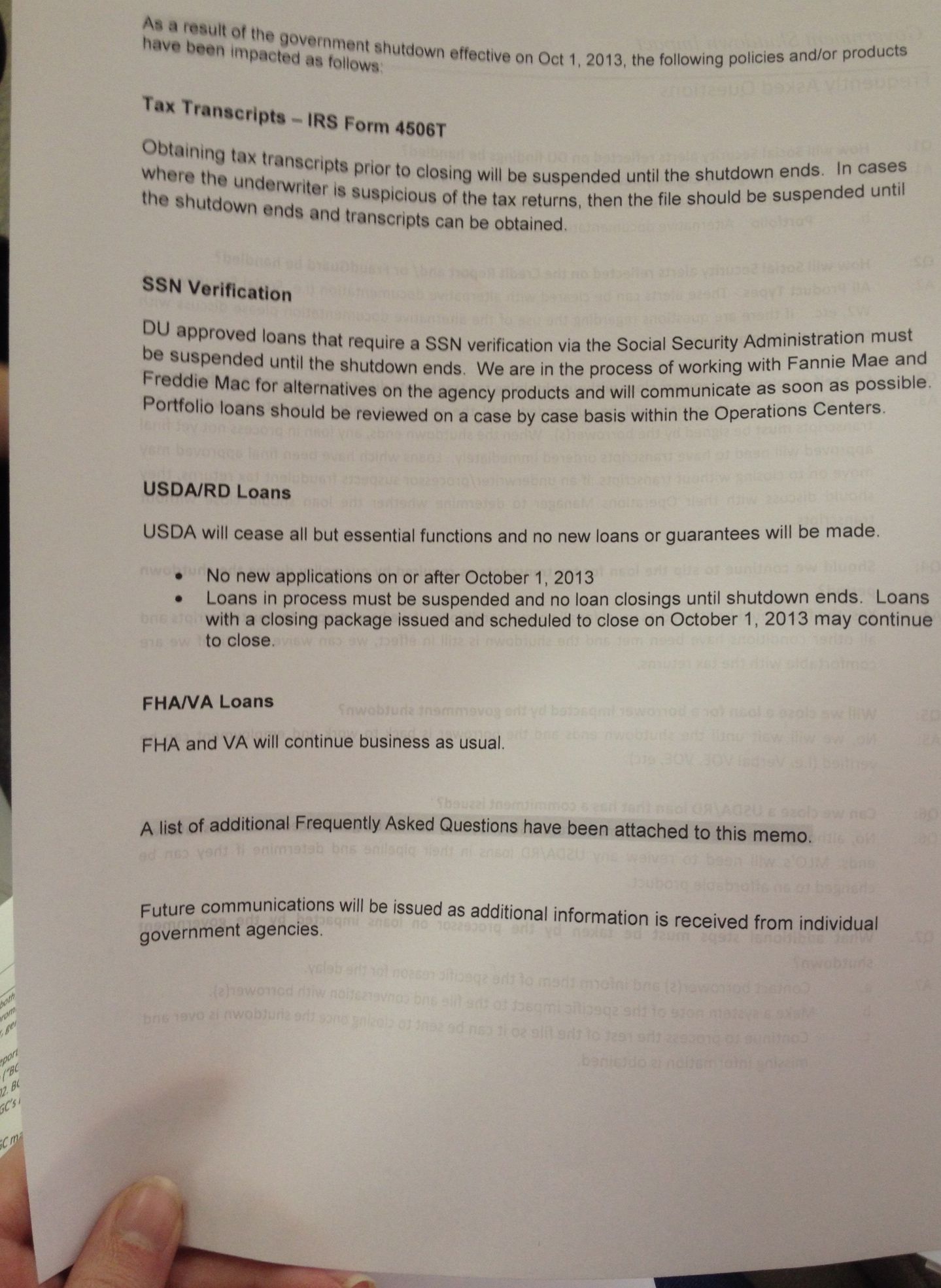

Anyway while we await the popping of yet another government-inflated mortgage balloon, the real estate industry is in full-fledged freakout mode over the partial government shutdown – specifically the impact it’s having on tax transcript processing, Social Security verification services, USDA/ RD loans and FHA/ VA loans.

Take a look …

(Click to enlarge)

Translation?

Good luck buying or selling a house during the #Shutdown.

17 comments

whew – glad we refinanced when we did

South Carolina Court Dismisses Foreclosure Based Upon U.S. Supreme Court Decision

Bill Sloan, Esq., in the 9th Judicial Circuit of Common Pleas in Charleston, South Carolina successfully turned the head of at least one judge, citing the United States Supreme Court case of Carpenter v Longen, 83 U.S. 271, 16 Wall. 271, 21 L. ed. 313 (1872).“Absent a loss , a claimant has suffered no injury. Unless a claimant can colorably assert a loss, it lacks standing. The point is that in the cloud of overlapping and duplicitous transactions that characterizes the claims of securitization and retreat from allegations of securitization, there remains a series of questions about who lost what, when and why — and that inevitably leads to questions of who owes what, when and why. The banks would have the courts treat these transactions as simple singling out one single event from dozens of related events — namely the point at which the borrower stopped making payments. They seek to misdirect the court away from an inquiry of whether the payment was due, or due to the claimant, or whether there was any loan at the base of the transaction chain.

Attorneys came into court saying they represented Deutsch Bank in the foreclosure — despite a very clear memorandum from Deutsch stating that nobody had authority to bring a foreclosure action in its name. The question of whether Deutsch even knew about the action was apparently never brought up. Instead the case turned on familiar arguments that the Trial Judge dispatched in a 4 page opinion and order.

http://livinglies.wordpress.com/2013/10/04/south-carolina-court-dismisses-foreclosure-based-upon-u-s-supreme-court-decision/

Merely having paperwork doesn’t mean you have a legitimate claim. The Court found that the Carpenter case from 130 years ago stated the requirements quite plainly. The Supreme Court decision “clearly supports the notion that the Plaintiff must own the Note and Mortgage at the time the Complaint was filed.” The Court was also obviously disturbed by the fact that MERS was the mortgagee but never mentioned in the note.

Translation: as close as I can get in lay terms the Court is merely stating the obvious. At least it was obvious before the Courts lost their way in the maze of legal arguments and procedures attempted by players in the cloud of false securitization claims.

If your lawsuit is based upon a loan you must allege that the loan was made. If your action is based upon acquisition of the loan you still must allege that the loan was made and that you actually paid for acquisition of the loan. Otherwise the claim is speculative and cannot invoke the jurisdiction of the Court. Without that the second requirement is impossible to meet — that you have suffered damages as a result of the making the loan and the borrower not repaying it. These are not mere empty recitals. Without them, no lawsuit can continue.

http://livinglies.wordpress.com/2013/10/04/south-carolina-court-dismisses-foreclosure-based-upon-u-s-supreme-court-decision/

The Wall Street cloud has argued that they can correct this during litigation. But this Court correctly said that is impossible. The basis for a trial in which the evidence would be presented would be the Complaint. If the Complaint requires that ownership of a real loan be present at the time the Complaint is filed then the Court’s jurisdiction has never been invoked. The Court has no choice. And the reason for this is that it is very well-settled that you bring a matter to court that must be an actual controversy and a plea for relief that can be legally granted. The fabrication of instruments after the filing of the lawsuit for the express purpose of the lawsuit is not only lacking in credibility it is clothed in impossibility.

The fact that the trial court cited a specific U.S. Supreme Court case from which the Supreme Court has apparently never retreated, means that the trial court was saying that this issue was decided 130 years ago, it is the law of the land and it overrides any state court that would rule otherwise.

This also lends support to those proactive homeowners who are “current” in making payments to a bank other than the originator who purports to be the servicer or the new owner of the loan. If they cannot answer the basic questions above as their response to a qualified written request or debt validation letter, then it is reasonable to assume that they are neither the lender nor the acquirer of the loan despite their representations to the contrary. Saying it doesn’t make it so.

http://livinglies.wordpress.com/2013/10/04/south-carolina-court-dismisses-foreclosure-based-upon-u-s-supreme-court-decision/

Thus payments received should be allocated to all the loan accounts in that tranche. To say otherwise would require a homeowner to default on a loan in order to get the allocation — obviously a result that any sane person would want to avoid. The sole assets of the tranche are the loans according to the Wall Street players and their paperwork. Hence the account receivable for each loan would be allocable to eachloan in the pool based upon some reasonable formula and not necessarily pro rata. The bankers take advantage of this complexity and serve themselves a full cup of fees in the “breakage” that results from the allocation of those payments. Then they serve themselves again by not informing the investor that money has been received because the bankers say that the money received was a proprietary trade of the bank.

In short they keep money that should have been allocated to the account receivable of the investor. By not doing that they cheated the investor. But the fact they were so obviously the agent of the investor means that wherever the money landed, it must, from the perspective of the borrower or other outsiders to the cloud, be allocated for purposes of computation of the real unpaid balance of the creditor, after taking into account amounts held by the agent for the investor regardless of whether the agent willingly gives it up.

It’s difficult but not impossible to follow. The bottom line is that most of the money from many of the loans ended up in the pocket of the bankers who were supposed to act merely as intermediaries. And by the sheer power of their influence to declare the insurance and the derivative securities and hedges to be neither insurance nor securities, they are allowed to insure the same asset over and over again, without ever reporting to the investor that the account receivable has been paid down. That is why bank profits are high while investors are reporting losses.

This results in the account payable of the borrower remaining as though no payment had been received. Since the payments received were explicitly not purchases, they can only be accounted for as loss mitigation payments not merely bets by underwriters who were betting against the same securities they were selling to pension funds and other investors like credit unions and other vulnerable institutions.

Thus we find ourselves in a rabbit hole where the courts are largely refusing to see what is front of them even when it is well presented. All we ask is that the Court require compliance with requirements of pleading and proof. The complex facts will be revealed as one layer after another is unveiled through discovery.

I thought you were a hacker, not a lawyer. Geez

Good. Dam good. Maybe the prices will drop further this time and I can actually buy value instead of hyper inflated pricing via realtors and lenders fees.

AND FRACKING TAXATION WITHOUT REPRESENTATION. See lexington rates by THE FRACKING SCHOOL BOARD.

SOUTH CAROLINA COURT HOLDS THAT FORECLOSURE LAW OF US SUPREME COURT TRUMPS EVERYTHING – FORECLOSING PARTY MUST “OWN” BOTH THE NOTE AND THE MORTGAGE.

BAMMMMMM!!!!!!!!!!!!!!!!!!!!

http://stopforeclosurefraud.com/2013/09/23/deutsche-bank-national-trust-company-v-heinrich-south-carolina-court-holds-that-foreclosure-law-of-u-s-supreme-court-trumps-everything-foreclosing-party-must-own-both-the-note-and-the-mortgage-to/

COPY OF JUDGE’S ORDER:

http://stopforeclosurefraud.com/wp-content/uploads/2013/09/Heinrich-Decision-South-Carolina-9-20-13.pdf

Thats not the story anonymouse. The story is more are coming. I dont care why they’re coming, just that they are. :)

Unfortunately there will be more wealth transfer from poor to rich people when this mini bubble busts.

Gov’t will use tax money for TARP-2 and justify it as “saving the system” once again.

Rich bankers will get even richer and middle class & poor people will get even poorer.

Even now, the bailed out banks that screwed up in the first place turn around with their reserves received from taxpayers, given to them by corrupt pols, and use that money to buy up the foreclosed homes and turn them into rental units for the same poor that lost houses in the first place.

It’s a sick, sick system…it needs to burn.

You think Pytel can comprehend all that on a Saturday?

Hes already three sheats to the wind!

Amen.

Bob Ewell: “What’s that got to do with it, Judge? I’m a God-fearin’ man. That Atticus Finch, he’s tryin’ to take advantage of me! You got to watch tricky lawyers like Atticus Finch!” – To Kill A Mockingbird (1962)

“Hedley Lamarr: Wait a minute… there might be legal precedent… Of course! Land-snatching!

[grabs a law book]

Land, land… ‘Land: see Snatch.’

[flips back several pages]

Ah, Haley vs. United States. Haley: 7, United States: nothing. You see, it can be done!”

– Mel Brooks’ Blazing Saddles

STUNNING RULING IN SOUTH CAROLINA – FRAUDSTERS ARE FORECLOSING WITHOUT OWNING THE NOTE – FORECLOSURE FRAUD – MAYBE NO MORE

SOUTH CAROLINA COURT HOLDS THAT FORECLOSURE LAW OF U.S. SUPREME COURT TRUMPS EVERYTHING: FORECLOSING PARTY MUST OWN BOTH THE NOTE AND THE MORTGAGE TO FORECLOSE

SEPTEMBER 20, 2013

In a stunning ruling from the Ninth Judicial Circuit Court of Common Pleas of Charleston, South Carolina, a Judge has issued a detailed, 4-page written opinion dismissing a foreclosure action filed by Deutsche Bank National Trust Company as the claimed trustee of an IndyMac securitization, holding that DB failed to show that it was the owner and holder of the original Note and Mortgage at the time the Complaint was filed. FDN South Carolina network counsel Bill Sloan, Esq. represents the homeowner and prepared and argued the homeowner’s Motion to Dismiss.

Counsel for DB made the familiar argument that it had possession of the original Note endorsed in blank, that the Note was a negotiable instrument under the UCC, that the Mortgage follows the Note, and that thus DB had established its right to foreclose. The Court disagreed, citing precedent from the United States Supreme Court’s decision in Carpenter v. Longan, 83 U.S. 271, 16 Wall. 271, 21 L.Ed. 313 (1872) which the Court found “clearly supports the notion that the Plaintiff must own the Note and the Mortgage to foreclose on the property (emphasis in the opinion).” The Court determined that “Plaintiff failed to show that it owned the Mortgage at the time the Complaint was filed”, and also noted that the Mortgage shows MERS to be the mortgagee but that “MERS is never mentioned in the Note.”

The Court stated: “It is clear that to have standing in this foreclosure case, Plaintiff must not only be the holder and owner of the original Note, but also the Mortgage as well. Plaintiff’s Complaint in this case fails to meet this criteria. Plaintiff lacks standing to initiate and prosecute the foreclosure, and dismissal pursuant to Rule 17(a) and Rule 12(b)(6) SCRCP is appropriate.”

This ruling is based on foreclosure law from the United States Supreme Court, which trumps any contrary state law which does not require the foreclosing Plaintiff to own both the Note and the Mortgage at the time that the foreclosure Complaint is filed. This ruling demonstrates the essential fallacy in the “UCC, I have the Note, mortgage follows the Note” theory espoused by every attorney for the banks and servicers. What remains to be seen is whether the judiciary handling foreclosure cases will follow the law of the U.S. Supreme Court or not.

A copy of the Order is available upon e-mail request.

Jeff Barnes, Esq., http://www.ForeclosureDefenseNationwide.com

SOUTH CAROLINA COURT HOLDS THAT FORECLOSURE LAW OF U.S. SUPREME COURT TRUMPS EVERYTHING: FORECLOSING PARTY MUST OWN BOTH THE NOTE AND THE MORTGAGE TO FORECLOSE

In a stunning ruling from the Ninth Judicial Circuit Court of Common Pleas of Charleston, South Carolina, a Judge has issued a detailed, 4-page written opinion dismissing a foreclosure action filed by Deutsche Bank National Trust Company as the claimed trustee of an IndyMac securitization, holding that DB failed to show that it was the owner and holder of the original Note and Mortgage at the time the Complaint was filed. FDN South Carolina network counsel Bill Sloan, Esq. represents the homeowner and prepared and argued the homeowner’s Motion to Dismiss.

Counsel for DB made the familiar argument that it had possession of the original Note endorsed in blank, that the Note was a negotiable instrument under the UCC, that the Mortgage follows the Note, and that thus DB had established its right to foreclose. The Court disagreed, citing precedent from the United States Supreme Court’s decision in Carpenter v. Longan, 83 U.S. 271, 16 Wall. 271, 21 L.Ed. 313 (1872) which the Court found “clearly supports the notion that the Plaintiff must own the Note and the Mortgage to foreclose on the property (emphasis in the opinion).” The Court determined that “Plaintiff failed to show that it owned the Mortgage at the time the Complaint was filed”, and also noted that the Mortgage shows MERS to be the mortgagee but that “MERS is never mentioned in the Note.”

The Court stated: “It is clear that to have standing in this foreclosure case, Plaintiff must not only be the holder and owner of the original Note, but also the Mortgage as well. Plaintiff’s Complaint in this case fails to meet this criteria. Plaintiff lacks standing to initiate and prosecute the foreclosure, and dismissal pursuant to Rule 17(a) and Rule 12(b)(6) SCRCP is appropriate.”

This ruling is based on foreclosure law from the United States Supreme Court, which trumps any contrary state law which does not require the foreclosing Plaintiff to own both the Note and the Mortgage at the time that the foreclosure Complaint is filed. This ruling demonstrates the essential fallacy in the “UCC, I have the Note, mortgage follows the Note” theory espoused by every attorney for the banks and servicers.

http://s355160796.onlinehome.us/category/lack-standing-to-foreclose/

Hah! ” … see Snatch … Haley …”

Brooks was always prescient like that.