PALMETTO STATE RESIDENTS FALLING FURTHER BEHIND …

South Carolina ranks second in the nation in terms of the percentage of its population with debt in collections – another troubling economic statistic for a state supposedly in the midst of a “recovery.”

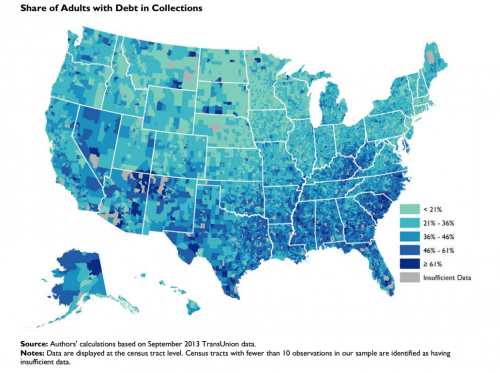

According to a study released this week by the Urban Institute, 46.2 percent of South Carolinians currently have debt in collections – second only to Nevada’s 46.9 percent. The national average is 35.1 percent.

Another 6.5 percent of Palmetto State residents have debt past due – well above the national average of 5.3 percent.

Want more bad news? South Carolina’s debt is also disproportionately large given our state’s income levels – which consistently rank among the lowest in the nation. The average debt in collections in South Carolina is $5,606 – well above the national average of $5,178.

Brutal, huh?

Nationally an estimated 77 million Americans have debt in collections – although the percentage of the population facing such financial issues doesn’t appear to have changed much over the past decade.

Here’s what that looks like on a nationwide map …

Ouch ..

Why is this happening? From the Associated Press …

Wages have barely kept up with inflation during the five-year recovery, according to Labor Department figures. And a separate measure by Wells Fargo found that after-tax income fell for the bottom 20 percent of earners during the same period.

Exactly … in fact we’ve written on that topic twice this week (HERE and HERE).

Look, we don’t blame South Carolina residents for this … we blame their “leaders.” If state government would let them keep more of their money and let the marketplace improve their educational outcomes … things would be much, much better.

59 comments

Welcome to the new India courtesy of Nikki Randhawa.Haley motherfuckers.

Funny, all of America’s economy (not just SC) has been in a free-fall since Nov. 2008 (what a co-inky-dinky?)….I’d love to replace our economy w/ India’s…they have adopted capitalism, while Obama is attacking it in the US. You sound like a Common Core government school student: Read: http://scdigest.blogspot.com/

Feel free to move to India. Call me if you need help packing your bags.

uptil I saw the draft 4 $5514 , I be certain that…my… cousin woz like actualey bringing home money parttime online. . there dads buddy has done this for only fourteen months and just cleared the dept on there appartment and purchased a great Fiat Multipla . For more information click FINANCIAL REPORT in ………………….. P????P.???

Not that I’m a big Haley fan but…personal debt is not caused by Haley, Obama or any politician.

Hey FITS: You’re re-trodding over beaten ground: This is B-O-R-I-N-G. The economy began slipping when Obama got elected. It has gone downhill since, and will not really correct until that some beech is out of office.

Meanwhile: a WAR is raging between the Parents and the media and education industry Fatcats. Isn’t education -School Choice- one of your BIG initiatives?..

Anway, for those who want to be informed properly, on the WAR: Read: http://scdigest.blogspot.com/

If we could find a way to sell ‘stupid’ in a jar, we could pay off everyone’s debts just from the mother load that is GT’s brain.

Stupid is quite the toxic contaminant, best to let it stay contained within his hardened skull.

Yeah, but people keep responding to his stupidity.

He seems to drive so many comments, I wonder if he and Emily Peterkin aren’t Sic by another name.

Black Helicopters much?….

Clue: thoughtful discourse, and enlightened opposition to ignorance, is interesting. Marching in lockstep bliss in support of constant failure, is BORING, and does not provoke response.

Black Helicopters much?….

Funny…you’re the scared one, Boo.

Every common bore article you write is about Cindi Ross Scoppe, damn GT you have a hard on for her. Did she turn you down?

Common mistake by people of your intellect. I reference Scoppe because she is an invaluable gauge of the liberal condition. Not only that, she is drawing out Spearman. this Common Core issue is a bare-knuckle fight of the people vs media-education industry control of our children. If we lose this now, the public schools are done. I have a charter school available, and I KNOW the leaders there DETEST Common Core and liberalism.

Aside from that: I’d actually vote for the Democrat, because then we can pin the rot on him, instead this dumb@$$ Spearman using the GOP label to damage the education system so her fat @$$ can get fatter.

And Spearman running to Scoppe, swearing allegiance to the left, is a MAJOR F*#k up on her part. We cannot allow that. Does that help clear it up for you?

nice

Useless information without breaking down the origination of such debt. Is it medical bills? Revolving credit? Mortgages (since in SC it can easily take 9 months to complete a foreclosure)? Student loans?

Willing to bet student loans alone add a sizable chunk.

Perhaps if we all clicked the links and learned how to make $7,500/month working part time—all from the convenience of our home—we could really put a dent in that number.

My mother-in-law made $10,000 last month with just 2 hours work per week!

Is her nickname “shop vac” or “Hoover”?

to clarify,

1) EX mother-in-law

2) “Windy”

yeah but she is a great dominatrix.

Just get a payday advance and title loan to pay off your credit cards. What could go wrong?

Oh man….don’t get me worked up this early. I have yet to swear on Fits….but payday and title loan places just might cause it to happen.

Why? Do they (“payday and title loan places”) hunt down poor people and force them to sign the loan documents (without letting them read said documents) while holding a pistol to their head?

Absolutely not. Never implied that. To extrapolate by comment like that is to make undue assumptions. But its a shoddy business at best…preys on those that are most vulnerable and, unfortunately, are not educated enough to understand the downward spiral and vicious cycle. If everyone wants to fuss about how many people remain on government assistance…..allowing these particular (quasi loan shark) businesses to continue to operate only encourages the continual assistance.

Finally, I think we can all agree that those beautiful converted KFC restaurants, etc., all painted in shiny yellow…you know, the ones with bullet proof glass inside…..aren’t exactly a positive sign of growth, development, and increased property values.

I did assume you were on the path to making the payday lenders the boogeyman. But in your refutation of my assumption are you not validating my assumption? The people that use those businesses may very well be uneducated, ignorant even, but they know damn well what they are getting into. And again, no one is holding a gun to their heads. Not unlike the people that buy the big, fancy homes they can’t afford figuring they will eat bean and weenies for a couple of years but can show off their new digs to friends in the meantime. They’ll cry a river that they were taken advantage of but I’ve seen and talked with some people that do that and they just figure they’ll default and to hell with paying it off (payday loan or house)

Sorry, no sympathy from me.

(1) Did not refer to them as anything close to a “boogeyman.” I stated its a shoddy business. I’m all for freedom to maneuver within the boundaries. However, would you want a strip club or adult toy store to build directly next to your business? Of course not (assuming you don’t run a business with synergistic interests). For the same reason, the market drives values and there is absolutely no reason to want those dreadful looking buildings around your principle place of business.

(2) Did not provide sympathy. For all you know my interests could be nothing other than selfish and greedy. For example, perhaps I am a real estate investor or developer. Maybe I have options on property adjacent to these buildings. Maybe I am speculating and want to merely fill my own pockets. Maybe I am not. But again, nothing in my text provides sympathy. Don’t draw the inference that I am advocating the “nanny state.”

(3) I never even remotely pretended to argue that they were being strong-armed or coerced into dealing with those industries. However, it is clearly a slippery slope (think Ponzi scheme) when you borrow an advancement because you aren’t financially wise, and merely borrow against a future obligation, such that, you will have to borrow again.

(4) I certainly am not sticking up for a person that is house poor. I agree everyone is a big boy/girl and can read financial documents. Additionally, I believe they can make decisions for themselves. But, wouldn’t you agree that it was a good thing that “some regulation” came in and curbed the ridiculousness that was the “no doc” loan for someone with a 520 credit score? I know I certainly do. There comes a point were people really toe the line of what is right and what is wrong when it comes to making a buck.

I have several acquaintances that run title loan business. They have explained the model to me. Quite fascinating how some can stoop so low to make money. But hey, its freedom…I get it.

Finally, I’ll repeat this. Most on here–regardless to political affiliation–agree that it would be a good thing to have less Americans on welfare. As such, I find it hard to believe that it wouldn’t increase the chances of reducing welfare payments if we removed an irresponsible temptation from the uneducated.

Finally, legislative history of our state proves that the G.A. has attempted to close down or significantly alter the title loan and payday advance industries. However, there’s a few grandiose political contributions that come from the upstate. Shockingly, these contributions come from someone who…wait for it…stands to benefit from this industry.

Sorry sport, everything you say about the payday lenders is derogatory and demeaning. Boogeyman is my wording but your words are implying such. Also, while you don’t specifically use the word sympathy your comments are crafted in a way as to gin up sympathy for those poor, poor people.

Again, no sympathy from me.

What about sympathy for the children of these uneducated people who sign these usurious loans?

While I don’t have much sympathy for *most* people who sign these loans, I still think those businesses are shady and unethical.

Wow. I had no idea it was almost 50% of the population.

Considering the medical billing industry is akin to the blind leading the blind, I’m guessing several percentage points can be chalked up to merely pathetic billing/accounts receivable practices.

It probably takes the average person about four seconds to find someone who has gotten an incorrect medical bill because their insurance company and the actual provider….oh, and the 3rd party billing entity… cannot get on the same page. You know, someone in a cubicle put “3PQ1F” in box 7a. They should have put “3PO1F.” Thus, after five months of poor customer service and $10.00 of postage used—-it will get corrected.

“Considering the medical billing industry”

Here’s how the medical billing and corrupt medical system here in SC works when you don’t have insurance:

1. You need some type of medical service, you get it, then get the bill afterwards.

2. After you get the bill and call them(the hospital), two things happen. 1st, after they confirm you don’t have insurance, you then get no “discount” that all the insurance companies get.

So if you are uninsured, you are automatically paying way more than someone that either has insurance or Medicaid, always at least 30% more, but usually 60% or more, especially at Lexington Medical for example.

As someone has said here before, “It’s expensive being poor.”

This crony capitalist event benefits several players, the Health Insurance companies(because they get special pricing that poor people don’t get), the hospital(assuming they get paid-a big assumption here in SC, although they do get write offs), and finally third party billing/collections.

See, once you tell them that you can’t afford a $20K bill for example, all at once, they immediately refer that to a debt collections agency. EVEN if you tell them you want to make payments, it BECOMES A DEBT COLLECTION EVENT.

So not only to the poor/uninsured people pay typically 60% more, they get to deal with a collections agency even if their intent is to pay, but over time…and of course it shows up as “debt in collections” for articles like the above.

It would really be interesting to overlay other demographics, such as race, gambling, unemployment, welfare, housing services, undocumented workers, density of payday loans, title loans, and rent-a-centers.

Yes we know its all the fault of the black folk. If we could just get rid of them and the brown folk, we could all be rich Republicans.

When did he say it was their fault?

So tell me, What is the value of overlying all those issues with race, unless you are trying to make a point about problems cause by people of a particular race? The exercise he proposes is meaningless otherwise.

Merely researching whether a certain problem like debt or poverty affects a race does not mean you’re blaming the race for debt and poverty.

You’re clearly not smart enough to comprehend the difference between blame and determining how a problem affects different groups of people.

Unlike you Tom, anyone can click my profile and see every comment I have ever made on Disqus. By doing so, it would be pretty hard to say the stupid shit you do. I have a real job (not a sock puppet, look in mirror for example), I don’t wholeheartedly endorse the Rs or the Ds (even though i must admit,Libs piss me off the most, with the Religious Right after that), and I usually vote for the person, not the party. In conclusion, your post reveals more of your racist ideas than mine, genius.

So you think I don’t have a real job? That tells me a lot about you. Republicans and Tea Partiers and people who call themselves conservatives assume people who disagree with them don’t work. They assume all successful people agree with them, and that people who don’t agree with them are freeloaders. I happen to work about 60 hours a week. I have never had a government job in my life.

But what was your point if not related to race? Of course debt is going to higher in areas with high unemployment. Of course unemployment among minorities is higher than unemployment among whites. So why do we need to overlay all those things with with race unless you are making a point about race.

And if we do such an overlay and find the obvious, that minorities have more debt than whites, what would be your point then, if not related to race?

The fact that you immediately assumed race was his issue says more about you than him Tom. We already know there are more white folks on welfare, in public housing etc.

There is no point to overlaying all those issues with race unless the point is about race. Race is the only factor that is immutable factor in the test. What would be the purpose of the exercise if not to seek correlation of the factors that change with the unchanging factor?

There is if you wish to address some of the problems via faith based initiatives or through social networking. I seem to recall that he actually suggested overlaying a variety of data, not just race. Every thing isn’t about the color of one’s skin. In fact, in reality, very little has anything to do with “race”.

You are really grasping a straws here. Lets at least stick to the most obvious reason for such a test. He suggested overlaying a variety of things prevalent in any area where there are a disproportionate number of poor people with race.

Why would one need a study to tell us unemployment, and gambling increase debt? Why do we need a study to tell us that payday loan centers, rent-a-centers, and title loan places crop up were poor people need to borrow money?

The purpose of such an exercise would be to link all these things to minorities; and as I said earlier, if you think conservatives are looking for information to devise better aid programs you are nuts. You’re fooling no one, by the way.

Who said anything about conservatives or democrats, Taz simply said “… it would be interesting…”. I would be interested in the clusters as well, not just race but in all of the categories he mentioned and a number of others as well. I spend money for some demo graphic mapping services to help target some of my activities.

Every post to Tom is Red or Blue. He’s on Yahoo yelling at people who comment “I like pizza” in response to a story about stock prices saying “WHY DO YOU HATE BLACK PEOPLE EATING PIZZA!!!111@!@1”

To figure out which communities need aid with debt. You seem dumb.

Oh for god sakes, did you grow up under a barrel or on another planet. You must be beyond dumb if you think “conservatives” are trying to determine if minorities need another aid program. Republicans have made minorities the scapegoat for the problems in this state for decades. If you listened only to Republicans you would think he entire federal deficit is cause by minorities getting food stamps.

(actual mentally challenged person)

Taz, I’ve dealt with Tom before. He always argues using ad hominems in an attempt to compensate for his lack fo wit.

Well you can’t prove it by looking at his past comments, and that was my point. Go on any disqus based site and you can always spot the sock puppet shills. They will never have any comment history and they have the most posts on any thread, all BS party talking points.

What do you expect in a state that allows predatory lending at rates up to 50%. It is illegal in most other states, but not here.

Check out that map and then overlay Red states. Boy – Red state governors sure provide a thriving economy for their constituents. Meanwhile in Blue land – —–

According to “Money Facts,” at the Bureau of Engraving and Printing’s website, the “defacement of currency is a violation of Title 18, Section 333 of the United States Code. Under this provision, currency defacement is generally defined as follows: Whoever mutilates, cuts, disfigures, perforates, unites or cements together, or does any other thing to any bank bill, draft, note, or other evidence of debt issued by any national banking association, Federal Reserve Bank, or Federal Reserve System, with intent to render such item(s) unfit to be reissued, shall be fined not more than $100 or imprisoned not more than six months, or both. Defacement of currency in such a way that it is made unfit for circulation comes under the jurisdiction of the United States Secret Service.

Assuming you are referring to the picture above this part of your post “with intent to render such item(s) unfit to be reissued” would negate the need for any law enforcement action.

Just being a smart ass…

Now if we can just open up a few casinos in Myrtle Beach maybe we’ll catch Nevada.

If Argentina had paid what they owe us, it would be a big help.

Argentina owes private entities money not the US government.

Wages in SC have dropped to 2003 levels. Then we have 75,000 illegal aliens living in SC that work for companies that circumvent the law – its a free for all. Lawlessness is in. Obeying the law has gone with the wind. And that holds true even for SC government. Just look at Bobby Harrell and his I-526 Boondoggle.